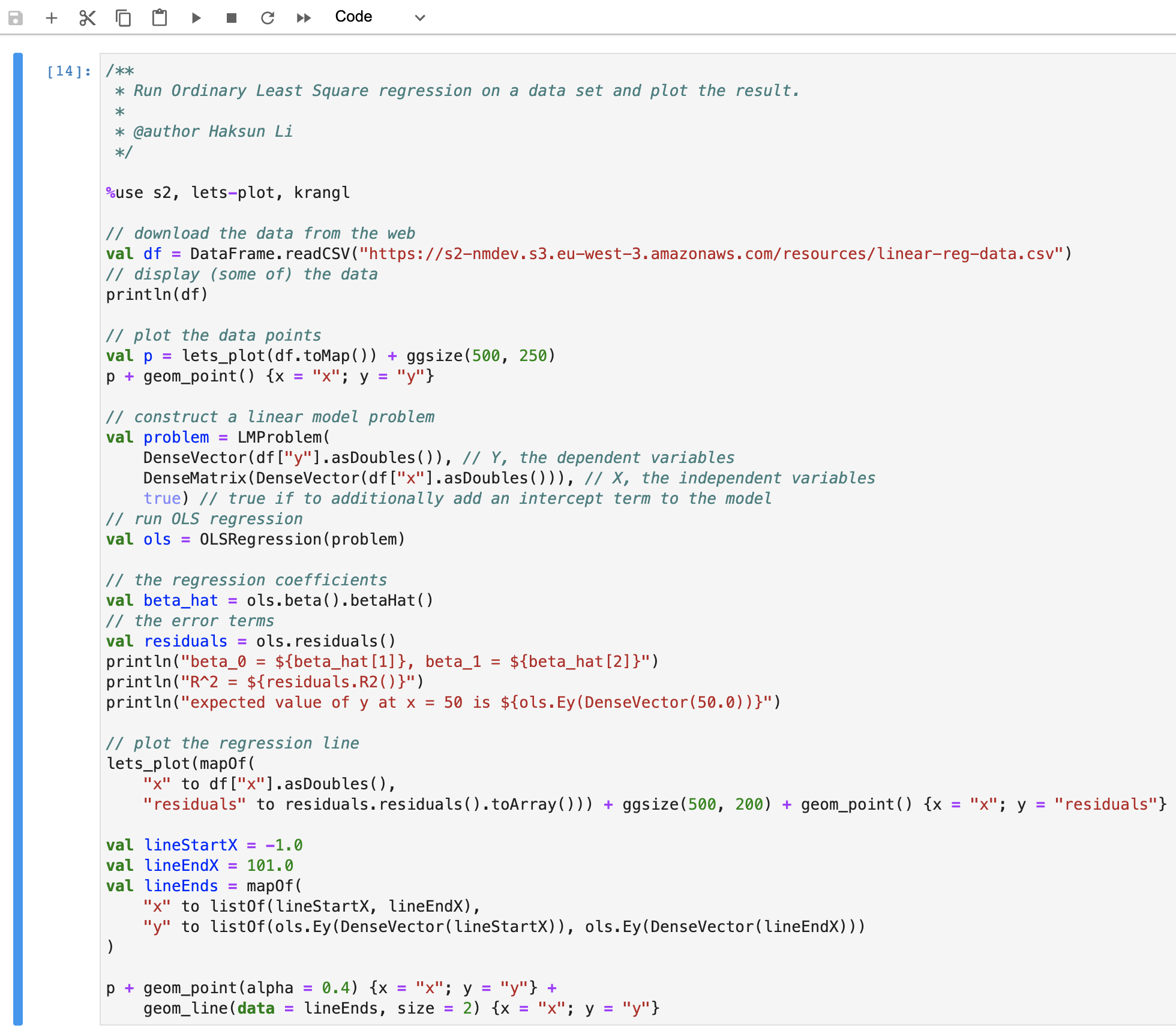

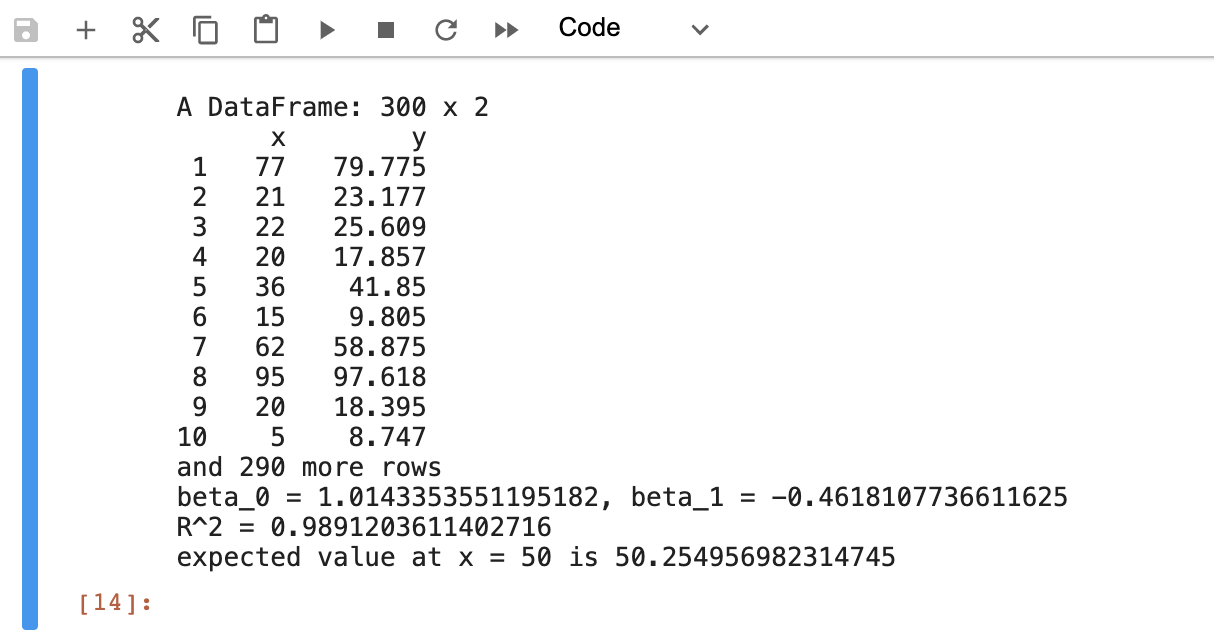

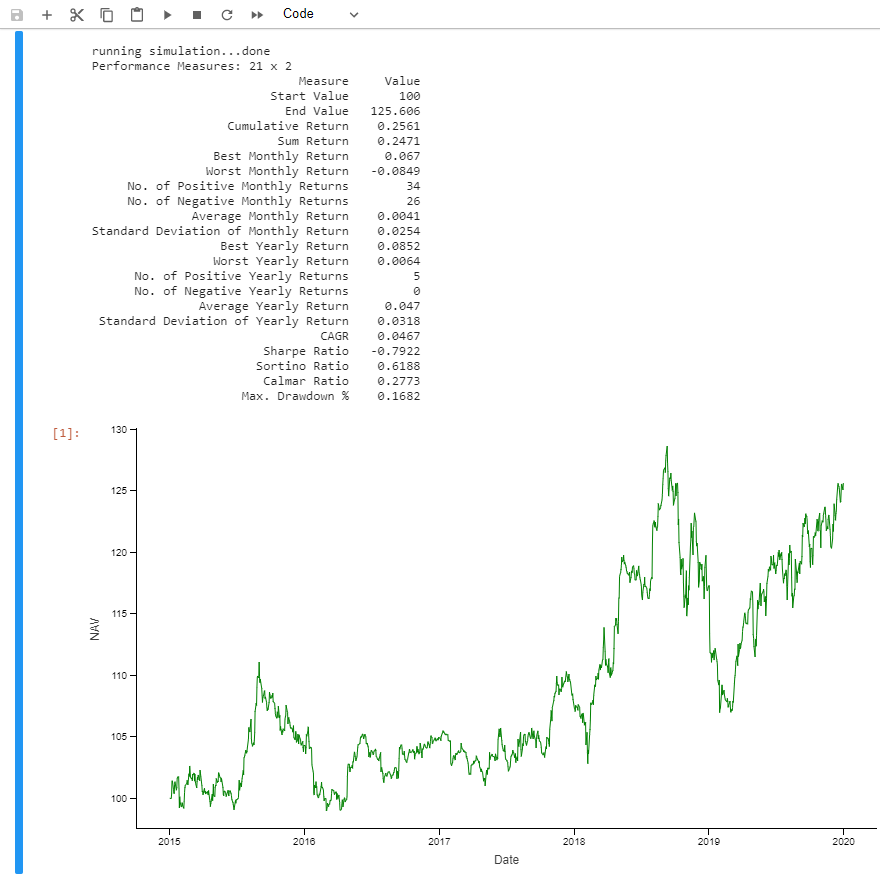

AlgoQuant is a large library of financial analytics. It has hundreds of functions. It also comes with well cleaned and professionally maintained data for equities (US and China). AlgoQuant has many templates and frameworks for users to do research in portfolio management.

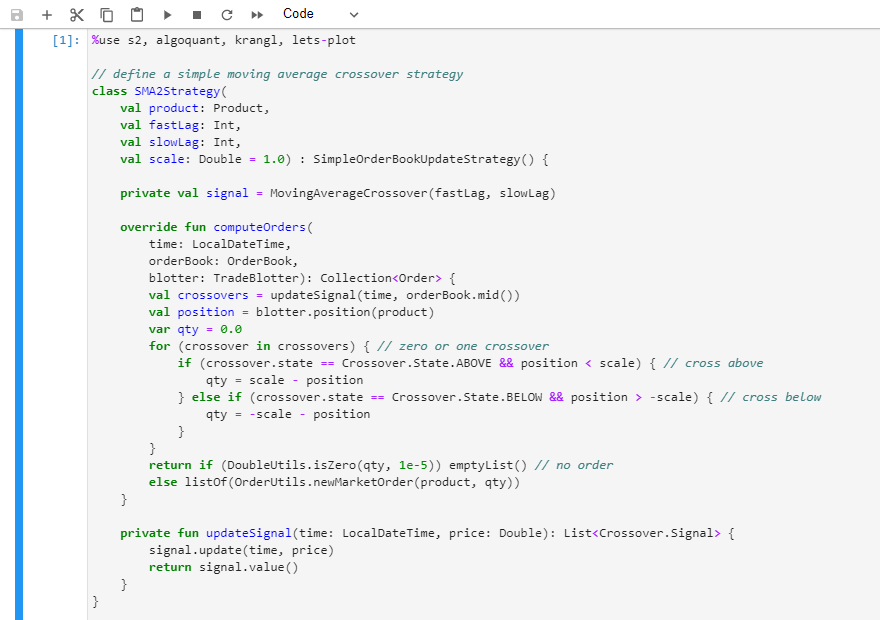

For example, suppose a user want to study how a simple moving average crossover works for a particular stock, s/he needs only to write the strategy code in a few lines.

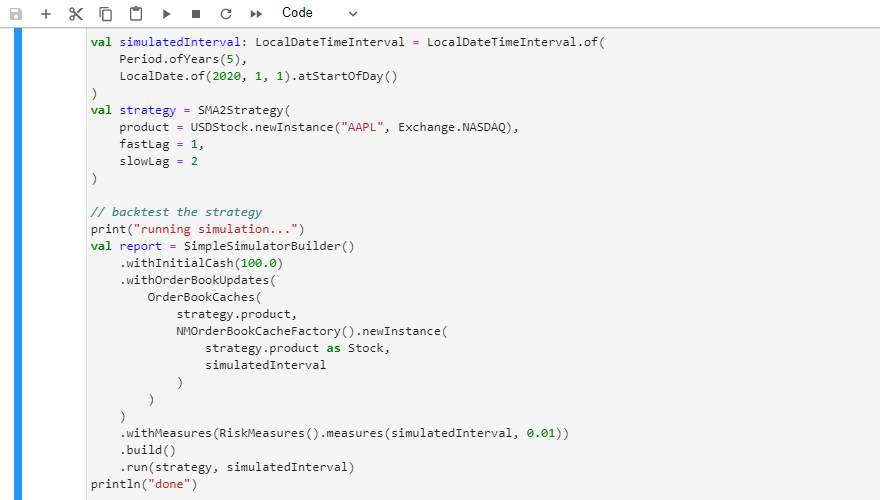

The script can be plugged into the AlgoQuant framework for backtesting.

AlgoQuant has a suite of analysis and reporting tools.

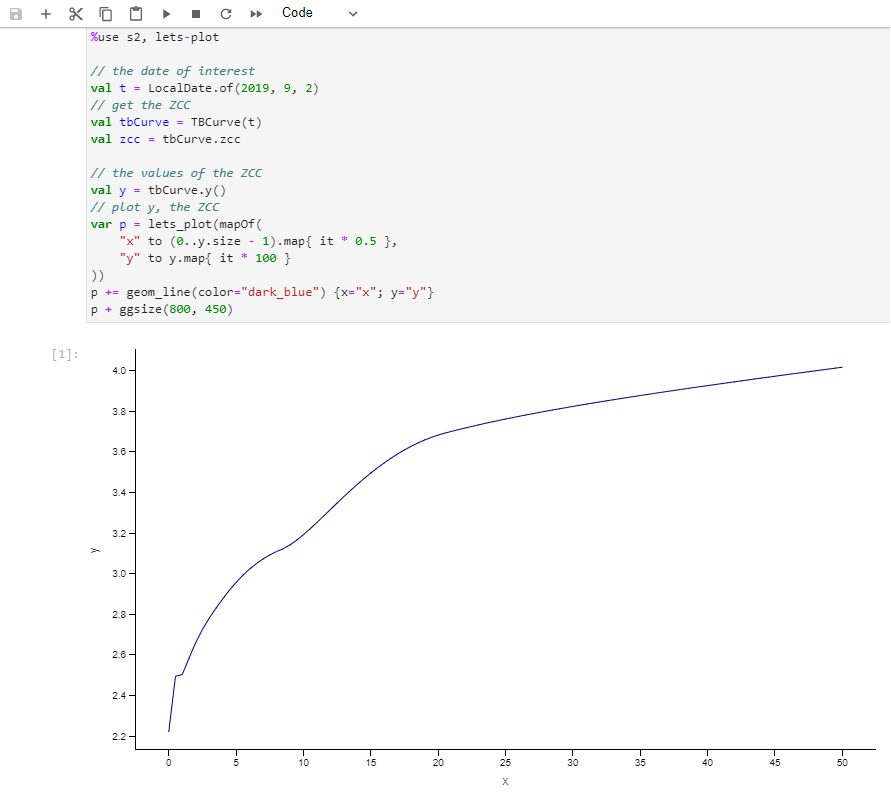

SuperCurve is a fixed income data firm in China. They sell high quality bond data and analytics.

A user can retrieve China bond data in S2 using the SuperCurve API. Here is how s/he can fit a zero-coupon yield curve using those bond data in S2 using only two lines of code.

With a yield curve, s/he can price any fixed income instrument on that date in S2.